from FoxNews,

10/15/22:

Sandpiles can be fun. Nothing beats taking kids to the beach (or being a kid!) and watching their creativity blossom into all kinds of magical shapes. The problem with sand construction is it doesn’t last. I have it on good authority that building your house on the sand probably won’t end well.

The same holds for financial sandpiles. The piles can grow quite large and then suddenly collapse with a single added grain of sand.

The point at which this happens is unpredictable. That it will happen is highly predictable.

We are in unprecedented times. A 60/40 portfolio of stocks and bonds is supposed to offset volatility in equity bear markets. To date, these “balanced” portfolios are down 21.3% this year, meaning they need a 27% return to get back to even. It’s even worse than that, because almost all pension funds have an inflation factor to keep up with.

Pension obligations, i.e. debt, are a significant part of the large and growing global debt load. They are big enough to have systemic effects all their own. This seems to be happening in the UK.

how years of falling interest rates raised pension liabilities—a big problem for plan sponsors and managers. Lower interest rates reduced the return on the bond portion of a pension fund. In a world of zero and negative interest rates, pension funds simply couldn’t make their target returns (typically 7% and sometimes more) when 40%+ of the portfolio was making 2‒3% (at best!).

It worked well until rates went higher… or, as Ben says, “until the math broke.” Now they all want to exit at once.

In effect, UK pensions are in a solvency crisis. Giant debtors are in danger of not being able to meet their obligations—not the pension benefits years from now, but margin calls due immediately. They are thus frantically trying to raise liquidity. Their combined efforts to sell UK government bonds all at once raised rates even further, aggravating the problem and creating new ones. The word “cascade” is quite accurate. Each step leads to another one, bigger than the last. As of this morning, it looks like the Bank of England is calming the market, but it serves to demonstrate how fragile the debt/leverage system is. We will know more next week.

US pensions use different hedging tools, so they don’t have the particular problem UK funds are enduring. But they’re still not in great shape.

The difference between US and UK plans is that US plans can buy government bonds in their home currency, which is also the global reserve currency, and is the world’s deepest and most liquid financial market. They don’t need they kind of derivatives that are exploding in London.

The bigger problem for US plans is low fixed income rates led them to fill their portfolios with riskier assets like stocks, real estate, venture capital, and assorted “alternative” investments.

“Everywhere you turn, the biggest players in the $23.7 trillion US Treasuries market are in retreat.

“From Japanese pensions and life insurers to foreign governments and US commercial banks, where once they were lining up to get their hands on US government debt, most have now stepped away. And then there’s the Federal Reserve, which a few weeks ago upped the pace that it plans to offload Treasuries from its balance sheet to $60 billion a month.

“If one or two of these usually steadfast sources of demand were bailing, the impact, while noticeable, would likely be little cause for alarm. But for every one of them to pull back is an undeniable source of concern.

Easy money sparked inflation which the Fed is (appropriately, in my view) trying to squelch with tighter policy. But that’s raising the Treasury’s borrowing costs and—maybe more to the point—strengthening the US dollar, which globalizes our problem.

We have grown accustomed to fiscal and monetary rescues in every crisis: 2000, 2008, 2020. That may not be an option next time.

Inflation Creates Massive Pension Problems

Many pension funds have an inflation adjustment, typically using some version of CPI. The Social Security Administration informed us this week that Social Security cost-of-living adjustment will be 8.7% in 2023. What was $1,194,842 trillion rose to $1,285,640 trillion. A $91 billion increase. In one year!

This is going to create a future crisis in the US which will, along with other policy problems, produce a crisis that makes the UK pension problems small potatoes. Coming to a theater near you in the not-too-distant future.

The Mercer/CFA Institute’s newest “Global Pension Index” report. Summary of 2022 results.

Pension obligations, i.e. debt, are a significant part of the large and growing global debt load. They are big enough to have systemic effects all their own. This seems to be happening in the UK.

how years of falling interest rates raised pension liabilities—a big problem for plan sponsors and managers. Lower interest rates reduced the return on the bond portion of a pension fund. In a world of zero and negative interest rates, pension funds simply couldn’t make their target returns (typically 7% and sometimes more) when 40%+ of the portfolio was making 2‒3% (at best!).

It worked well until rates went higher… or, as Ben says, “until the math broke.” Now they all want to exit at once.

In effect, UK pensions are in a solvency crisis. Giant debtors are in danger of not being able to meet their obligations—not the pension benefits years from now, but margin calls due immediately. They are thus frantically trying to raise liquidity. Their combined efforts to sell UK government bonds all at once raised rates even further, aggravating the problem and creating new ones. The word “cascade” is quite accurate. Each step leads to another one, bigger than the last. As of this morning, it looks like the Bank of England is calming the market, but it serves to demonstrate how fragile the debt/leverage system is. We will know more next week.

US pensions use different hedging tools, so they don’t have the particular problem UK funds are enduring. But they’re still not in great shape.

The difference between US and UK plans is that US plans can buy government bonds in their home currency, which is also the global reserve currency, and is the world’s deepest and most liquid financial market. They don’t need they kind of derivatives that are exploding in London.

The bigger problem for US plans is low fixed income rates led them to fill their portfolios with riskier assets like stocks, real estate, venture capital, and assorted “alternative” investments.

“Everywhere you turn, the biggest players in the $23.7 trillion US Treasuries market are in retreat.

“From Japanese pensions and life insurers to foreign governments and US commercial banks, where once they were lining up to get their hands on US government debt, most have now stepped away. And then there’s the Federal Reserve, which a few weeks ago upped the pace that it plans to offload Treasuries from its balance sheet to $60 billion a month.

“If one or two of these usually steadfast sources of demand were bailing, the impact, while noticeable, would likely be little cause for alarm. But for every one of them to pull back is an undeniable source of concern.

Easy money sparked inflation which the Fed is (appropriately, in my view) trying to squelch with tighter policy. But that’s raising the Treasury’s borrowing costs and—maybe more to the point—strengthening the US dollar, which globalizes our problem.

We have grown accustomed to fiscal and monetary rescues in every crisis: 2000, 2008, 2020. That may not be an option next time.

Inflation Creates Massive Pension Problems

Many pension funds have an inflation adjustment, typically using some version of CPI. The Social Security Administration informed us this week that Social Security cost-of-living adjustment will be 8.7% in 2023. What was $1,194,842 trillion rose to $1,285,640 trillion. A $91 billion increase. In one year!

This is going to create a future crisis in the US which will, along with other policy problems, produce a crisis that makes the UK pension problems small potatoes. Coming to a theater near you in the not-too-distant future.

The Mercer/CFA Institute’s newest “Global Pension Index” report. Summary of 2022 results.

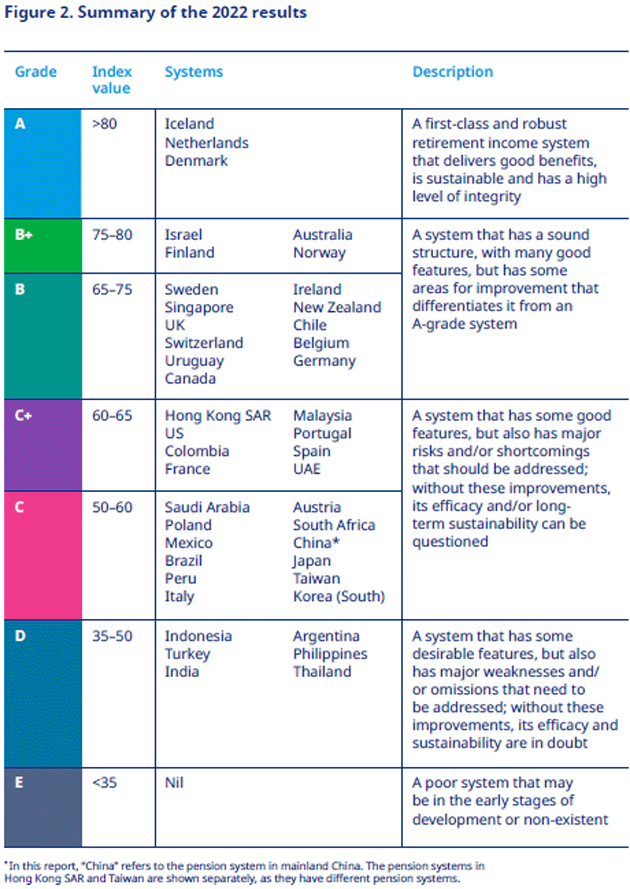

Congratulations, workers and retirees of Iceland, Netherlands, and Denmark. Your systems are “first-class and robust.” They’re also relatively small.

The US and France get a C+, meaning “major risks and/or shortcomings.” Going even lower, we see some very large economies in the C and D categories: Mexico, Brazil, Italy, China, Japan, Taiwan, South Korea, Turkey, India, Argentina.

“Efficacy and sustainability are in doubt” is a very kind way of saying, “You folks are in trouble.” The US has serious problems, but we also have serious capabilities.

I know many, perhaps most of my readers are fortunate enough not to depend on someone else’s pension promises. But you do depend on someone’s promises.

Congratulations, workers and retirees of Iceland, Netherlands, and Denmark. Your systems are “first-class and robust.” They’re also relatively small.

The US and France get a C+, meaning “major risks and/or shortcomings.” Going even lower, we see some very large economies in the C and D categories: Mexico, Brazil, Italy, China, Japan, Taiwan, South Korea, Turkey, India, Argentina.

“Efficacy and sustainability are in doubt” is a very kind way of saying, “You folks are in trouble.” The US has serious problems, but we also have serious capabilities.

I know many, perhaps most of my readers are fortunate enough not to depend on someone else’s pension promises. But you do depend on someone’s promises.

More From Maudlin Economics:

{kind=link}